Materials prepared by Susan Dambekaln, COO and Co-Founder, Capital Innovations LLC

The infrastructure sector is at the center of global disruptions, including shifts in available capital, supply chain disruptions, evolving societal and environmental priorities, as well as rapid urbanization. In recent years, the global pandemic has posed an entirely new set of challenges with the full effects still uncertain and undoubtedly playing out worldwide for many years to come. Infrastructure is critical as a foundation in building and sustaining resilient societies. Services such as communications, transportation, energy, water, sanitation and healthcare are broadly relied on in times of crisis.

Long-term economic growth has continually been linked to infrastructure development. In developed markets, there are considerable opportunities to renew existing infrastructure (i.e., roads, rail, hospitals, etc.) and to accelerate technologies such as 5G and renewable energy. In emerging markets, the need for significant investment in both traditional and digital infrastructure is vast.

WHAT IS INFRASTRUCTURE?

Infrastructure is a catalyst which improves living standards and economies globally. Simply defined, infrastructure assets represent a broad mix of the large-scale public and private systems, services, and facilities of a country or region that are necessary for economic activity to function. Some examples of infrastructure include power generation and transmission including renewable energy, water supplies and wastewater treatment, public transportation, rail, roads, bridges, tunnels, ports, airports, telecommunications, and finally, basic social services such as schools and hospitals.

Infrastructure has emerged as its own differentiated asset class providing distinctive investment characteristics. Part of what defines infrastructure assets is that they provide necessary goods or services to society, and they often have monopolistic positions in their markets with high barriers to entry. Given these characteristics, infrastructure assets tend to be highly regulated, resulting in investments with distinct qualities.

Infrastructure assets are usually built to have long useful lives because they provide a vital service and are expensive to construct. Additionally, the demand for the output from these assets tends to be inelastic given the scarcity of the resource being offered. With the pricing power that results from their position in the market, the revenue growth from these assets typically is limited to the rate of inflation by regulators. These factors may result in infrastructure investments being able to offer long-term stable cash flows that have the potential for hedging inflation.

Another characteristic of infrastructure investments is that they regularly exhibit a hybrid nature of fixed income cash flows coupled with capital gains. In addition, these assets can be improved, and their capacity can be expanded allowing for their principal value to grow over time. An opportunity for capital gains comes from investments involving development risk or monopoly businesses.

Finally, infrastructure investments offer a variety of risk and return profiles. Infrastructure investments range from low-risk regulated assets to moderate-risk loosely regulated entities such as energy production. These assets have the potential to hedge inflation and offer different levels of vulnerability to economic cycles. It is important to note that although these assets are all considered the same asset class, not all of them will exhibit the same risk and return behavior.

“Investing in global infrastructure can enable investors to further diversify their portfolios with an income generating asset class that typically exhibits a low correlation to traditional investments while offering a hedge from inflationary pressures.”

SECULAR TRENDS DRIVING DEMAND

Global demographic trends are driving the need for infrastructure construction in the world’s developing economies. China and India have shifted from agrarian to industrial and urban societies. These countries require new, modern infrastructure to facilitate the expansion of industry, the urbanization of their economies, and the effects of continued population growth and an expanding middle class.

In most developed markets, basic infrastructure is worn and dilapidated, having been constructed in the middle of the twentieth century. In these markets, the percentage of gross domestic product (GDP) that is spent on infrastructure has been declining steadily for decades, leaving a crumbling legacy. A vast majority of old infrastructure needs to be either repaired or replaced.

The Organization for Economic Co-operation and Development projects the level of investment needed to meet growing worldwide infrastructure demand will equal 3.5 percent of world GDP through the year 2030 – totaling more than US $55 trillion. The areas in greatest need of investment are the development and modernization of roads, power networks, water systems, and telecommunication networks.

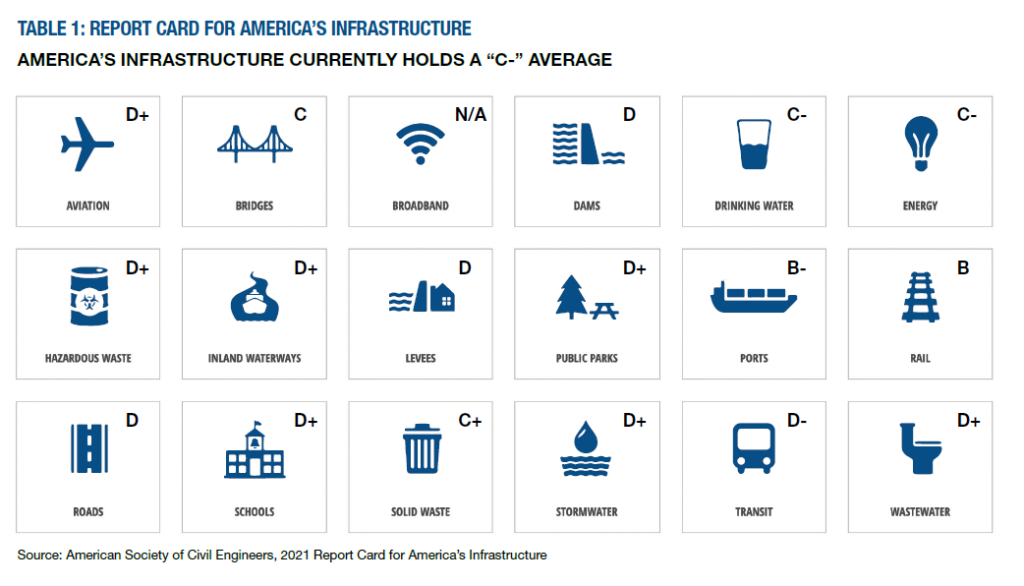

The amount of investment that is required to fix or upgrade existing infrastructure in developed economies is truly stunning, especially when one examines the state of infrastructure in the United States. The American Society of Civil Engineers has estimated that U.S. infrastructure funding needs are $5.9 trillion over a ten-year period from 2020 to 2029.

Source: National_IRC_2021-report.pdf infrastructurereportcard.org.

Even more disconcerting, funding levels as a share of all federal expenditures are exactly the same as they were more than 20 years ago. The United States’ crumbling infrastructure has been well documented over the past few years (see table 1). The ready supply of capital for projects is dwarfed by the demand for infrastructure, which is driven by the following:

- Population growth

- Urbanization

- Aging infrastructure

- Favorable economic and political climates

Over the years, the U.S. government has pushed the responsibility for the growth and upkeep of infrastructure down to the state level. The states have found that they have been unable to meet the capital requirements of this task. Real estate taxes, income taxes, and sales taxes all have declined precisely when the need for capital is the greatest. With the states’ inability to incur a budget deficit from year to year, they are unable to generate the capital for essential improvements to their infrastructure. The states are at a crossroads, and many are now beginning to court private investors to fill their budget gaps.

THE INFLATION REDUCTION ACT AND THE INFRASTRUCTURE INVESTMENT AND JOBS ACT

Fast forward to today’s politics. On August 16, 2022, the Inflation Reduction Act “(IRA)” was signed into law after a long path through Congress. As it relates to infrastructure, the package includes $386 billion of climate and energy spending and tax breaks – mainly for new or expanded tax credits to promote clean energy generation, electrification, green technology retrofits for homes and buildings, greater use of clean fuels, environmental conservation, and wider adoption of electric vehicles, among other purposes.

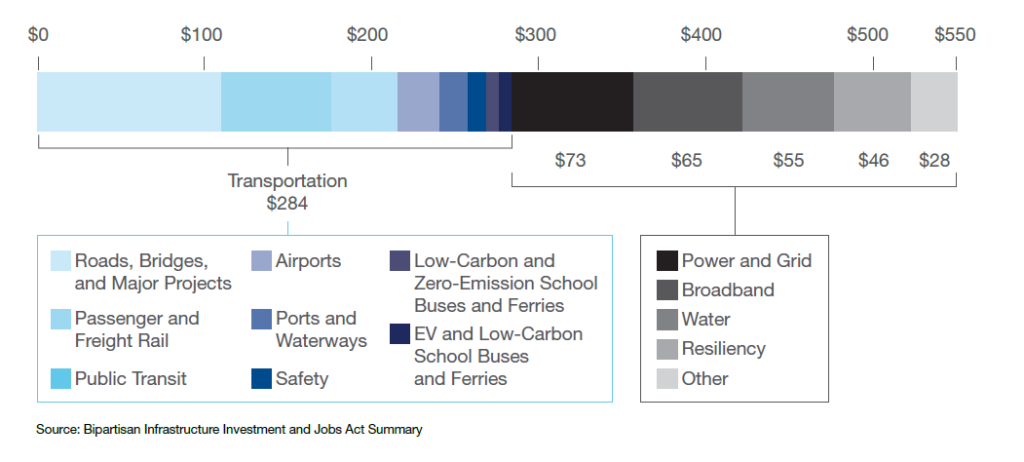

In addition, on August 10, 2021, the U.S. Senate passed and on November 5, 2021, the House passed the Infrastructure Investment and Jobs Act (IIJA), also known as the Bipartisan Infrastructure Act, which extends current transportation authorization legislation and related fuel excise taxes while increasing current funding levels by $550 billion over the next ten years. With the addition of $550 billion in new funding, the overall package provides $1 trillion over ten years for infrastructure improvements that include highways, bridges, waterways, transit, airports, the electric grid, and broadband.

Not surprisingly, the greatest amounts of funding are in areas that the federal government already funds, like highways and public transit. However, we note some areas that currently receive relatively little federal funding would see a more substantial boost under the IIJA. For example, federal funding for water and sewer projects would increase from only around $4 billion currently to around $16 billion by the middle of the decade. Additionally, the Biden Administration and congressional Democrats have linked the infrastructure bill to climate-related issues reflected in funding for clean energy, energy efficiency, and electrification.

AMONG THE PROVISIONS OF THE IRA:

- $161 billion for Clean Electricity Tax Credits

- $40 billion toward Air Pollution, Hazardous Materials, and Infrastructure

- $37 billion to Individual Clean Energy Incentives

- $37 billion for Clean Manufacturing Tax Credits

- $36 billion to Clean Fuel and Vehicle Tax Credits

- $35 billion earmarked for Conservation, Rural Development and Forestry

- $27 billion toward Building Efficiency, Electrification, Transmission, Industrial, DOE Grants and Loans

- $14 billion in Other Energy and Climate Spending

Source: Estimated Budgetary Effects of H.R. 5376, the Inflation Reduction Act of 2022 (cbo.gov)

THE IIJA ADDED $550 BILLION IN NEW SPENDING OVER FIVE YEARS

WHAT IS THE INFRASTRUCTURE OPPORTUNITY?

The global growth dynamics and a resolute need for modernization are expected to continue to drive investment in infrastructure worldwide. Population regions in Latin America, China, and India are experiencing infrastructure investment growth over multiple sectors including regulated utilities, transportation, and social infrastructure. This growth is necessary for these regions to accommodate their burgeoning populations.

Allocations. Increased allocations to the infrastructure sector are expected from pension funds and sovereign wealth funds among other investors given the risk-adjusted returns available compared to broader fixed income and securities markets.

Government actions. During the pandemic, a considerable amount of stimulus was injected into numerous economies around the world. In some jurisdictions, stimulus was directed toward a variety of infrastructure programs to aid economic recovery and broader-based economic multipliers. On the horizon is the potential for asset sales from governments as well as an increased focus on public-private partnerships to help balance their increased financing strategies.

Transport volumes. Transportation infrastructure ranges from meaningful recovery trades with transit systems and toll roads to comparatively less volumetric growth from rails and ports.

Ramped-up renewables. Across the globe, there is a significant focus on accelerating the growth of renewable energy generation and storage to accelerate the energy transition.

Carbon and hydrogen. The price of carbon remains in focus and the continued efforts toward widespread hydrogen utilization are major restructuring themes.

Data focus. The 5G and data infrastructure trends remain robust across the globe and tend to offer greater than traditional infrastructure growth rates.

Natural networks. Larger scale network owners (electricity, gas, hydrocarbons, etc.) and North American energy infrastructure owners facilitating exports from the continent (across all hydrocarbons) are well positioned for ongoing growth given changing supply-demand patterns.

KEY TAKEAWAYS – THEMES DRIVING OPPORTUNITIES

Long-term infrastructure investment is expected to surround the following themes:

Modernization: Billions of dollars are expected to flow to road, bridge, rail and other modernization projects, with significant implications for businesses that depend on this infrastructure.

Decarbonization: A drive toward a more sustainable economy powered by low-carbon alternatives—including wind, solar, hydropower and nuclear—considered to be in the national interest.

Security (focusing on both essential services and information infrastructure): Cybersecurity is not optional. Upgrades to networks and investing to better secure power, water, and social infrastructure.

Digitization: As digital technologies expand and the number of connected devices increases, the amount of data generated is anticipated to grow exponentially.

ABOUT CANTOR FITZGERALD, L.P.

Cantor Fitzgerald, with over 12,000 employees, is a leading global financial services group at the forefront of financial and technological innovation and has been a proven and resilient leader for 77 years. Cantor Fitzgerald & Co. is a preeminent investment bank serving more than 5,000 institutional clients around the world, recognized for its strengths in fixed income and equity capital markets, investment banking, SPAC underwriting and PIPE placements, prime brokerage, asset management, commercial real estate, infrastructure and for its global distribution platform. Cantor Fitzgerald & Co. is one of the 24 primary dealers authorized to transact business with the Federal Reserve Bank of New York. For more information, please visit: www.cantor.com.

ABOUT CAPITAL INNOVATIONS LLC

Founded in 2007, Capital Innovations is a leading alternative investment asset manager and has advised, managed, or co-sponsored investment programs encompassing over $9 billion in real assets including infrastructure, real estate and natural resources. Capital Innovations’ real assets investment solutions primarily include two groups of complementary products: actively managed listed and tax-advantaged private markets strategies. Additional information is available at www.capinnovations.com.