In a world of an increasingly concentrated stock market and growing economic activity in private markets, sophisticated investors need new avenues for diversification, yield, return, and access. Interval funds can provide transparent, tax efficient, and investor-friendly exposure to private markets in ways previously beyond reach.

This guide answers essential questions investors should ask when considering interval funds:

- What are interval funds and how do they differ from other investment vehicles?

- What are the potential benefits and risks?

- What asset classes can they provide access to?

- What are the key considerations, such as liquidity and fee structures?

What are Interval Funds?

Interval funds are a type of closed-end fund registered under the Investment Company Act of 1940 (the “1940 Act”). They combine aspects of both open-end and closed-end funds. A defining feature—and the source of their name—is that they offer limited liquidity to investors, typically allowing redemptions only at set intervals (e.g., quarterly). This structure enables interval funds to invest in less liquid, private market asset classes—including infrastructure, real estate, energy, private equity, and private credit—while still providing periodic access to capital.

They also offer some investors a gateway to these specialized asset classes with low minimums ($25,000 is typical). Many of the investments an interval fund makes would otherwise only be available to institutional and ultra-high-net-worth investors via private vehicles with minimums often between $5 million and $25 million. An individual trying to build a diversified portfolio across private market asset classes may need to commit upwards of $50 million to $100 million.

Finally, interval fund access does not require qualified purchaser ($5 million of investable assets) status. Some interval funds do not even require accredited investor status ($1 million net worth excluding primary residence or certain income tests), making them accessible for nearly all investors.

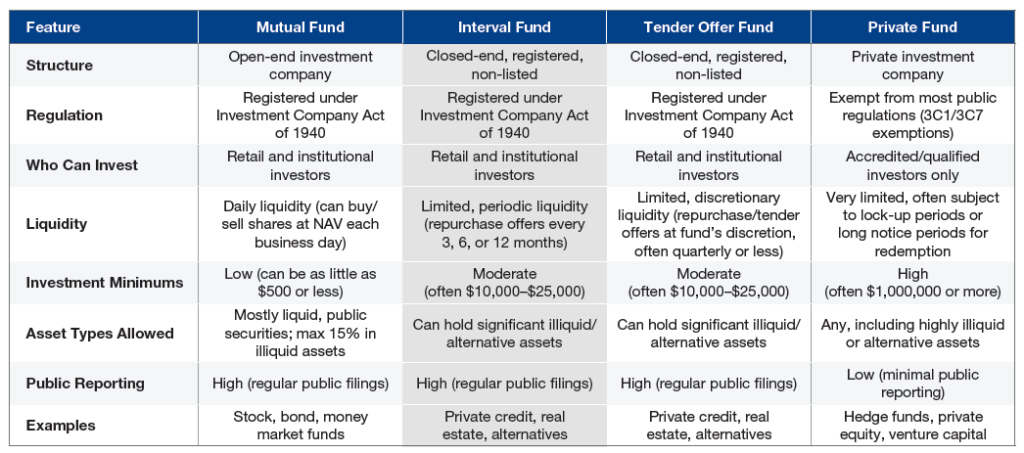

Fund Structures and Features

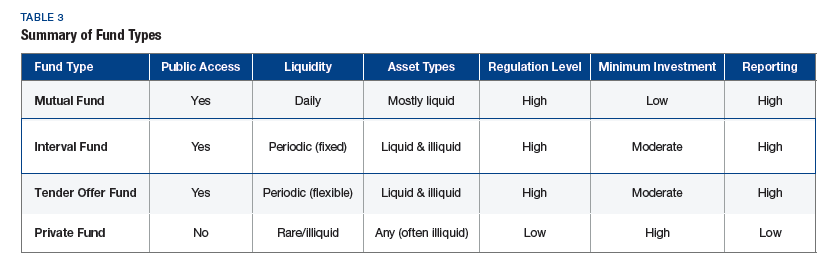

The table below compares key characteristics of mutual funds, interval funds, tender offer funds, and private funds, helping investors understand how these structures differ in liquidity, investor eligibility, asset flexibility, and reporting requirements.

How Interval Funds Work

Interval funds are a type of semi-liquid investment vehicle. Unlike mutual funds or exchange-traded funds (ETFs), they do not trade on public exchanges and do not issue or redeem shares on a daily basis. Instead, investors purchase and redeem shares directly from the fund at net asset value (NAV), which is typically calculated daily based on the valuation of the underlying assets. Unlike traditional closed-end funds, interval funds continuously offer new shares rather than relying on a one-time capital raise.

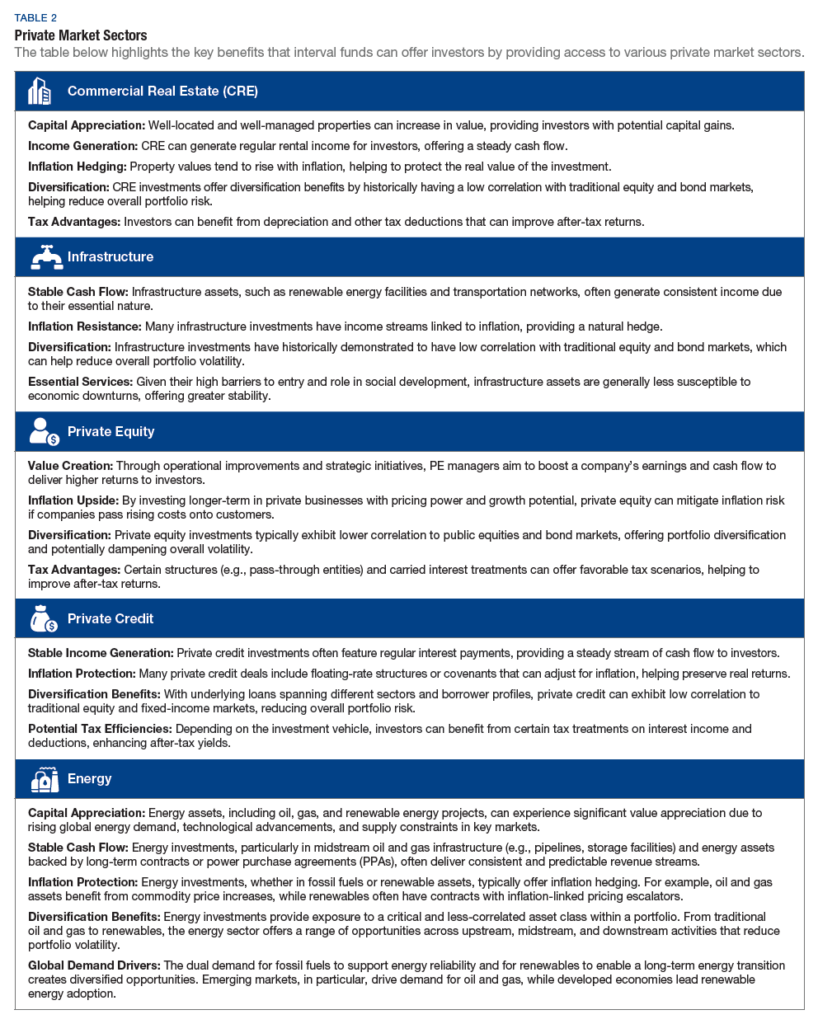

A key advantage of interval funds is their ability to invest in less liquid private market assets—such as infrastructure, private credit, private equity, real estate, and energy—while still providing investors with periodic access to capital. These investments can enhance diversification and typically exhibit lower correlation to public equity and bond markets.

As registered investment vehicles under the Investment Company Act of 1940, interval funds must adhere to strict standards around transparency, valuation, liquidity management, and investor communication. Fund managers are required to use rigorous valuation practices—often with third-party support—to determine the fair value of illiquid holdings. These practices, combined with regulatory oversight, offer a level of transparency often lacking in other private investment structures.

Interval funds provide limited liquidity by offering to repurchase shares at set intervals, typically quarterly. During these repurchase windows, investors may redeem a portion or all of their holdings at NAV, subject to fund-level limits.

To ensure fair and predictable liquidity, interval funds are required to disclose their repurchase policies in offering documents and must maintain liquid assets sufficient to meet redemption commitments. By rule, they must offer to repurchase at least 5% and no more than 25% of their outstanding shares at each interval, with 5% being most common. If redemption requests exceed the available amount, shares are redeemed on a pro-rata basis.

Definitions

- Mutual Fund: Pooled investment vehicle available to the public, investing in stocks, bonds, or other securities

- Interval Fund: A type of closed-end fund that does not trade on exchanges but continuously offers shares at NAV

- Tender Offer Fund: A closed-end, non-listed registered fund, similar to interval funds in structure but with repurchase offers made at the fund board’s discretion

- Private Fund: An investment fund that is not offered to the general public and is exempt from most public fund regulations

The Benefits of Interval Funds

Interval funds allow investors to access investments that may have previously been inaccessible or only available via private partnerships with material net worth and minimum investment thresholds. They offer access to strategies, managers, and markets that may otherwise be inaccessible for most people, including high-net worth individuals.

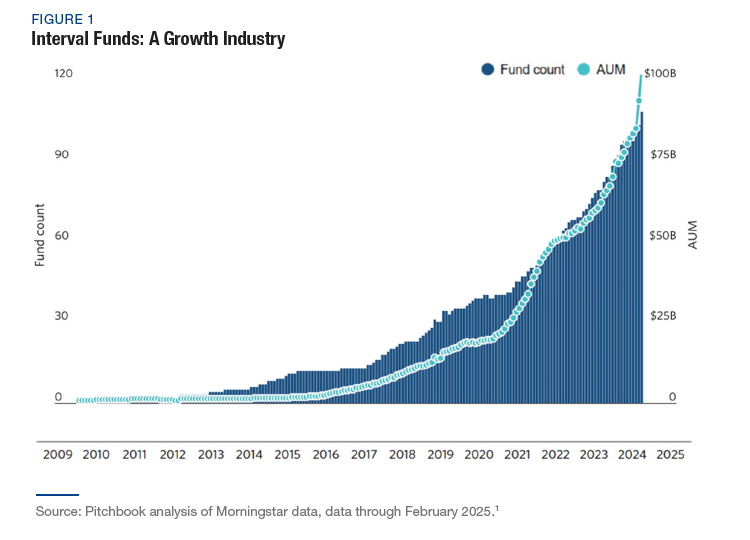

Historical Context and Growth

Interval funds have experienced rapid growth, especially over the last decade. According to Morningstar, interval funds have grown by nearly 40% year-over-year, reaching over $80 billion in assets under management.

Access to Private Markets

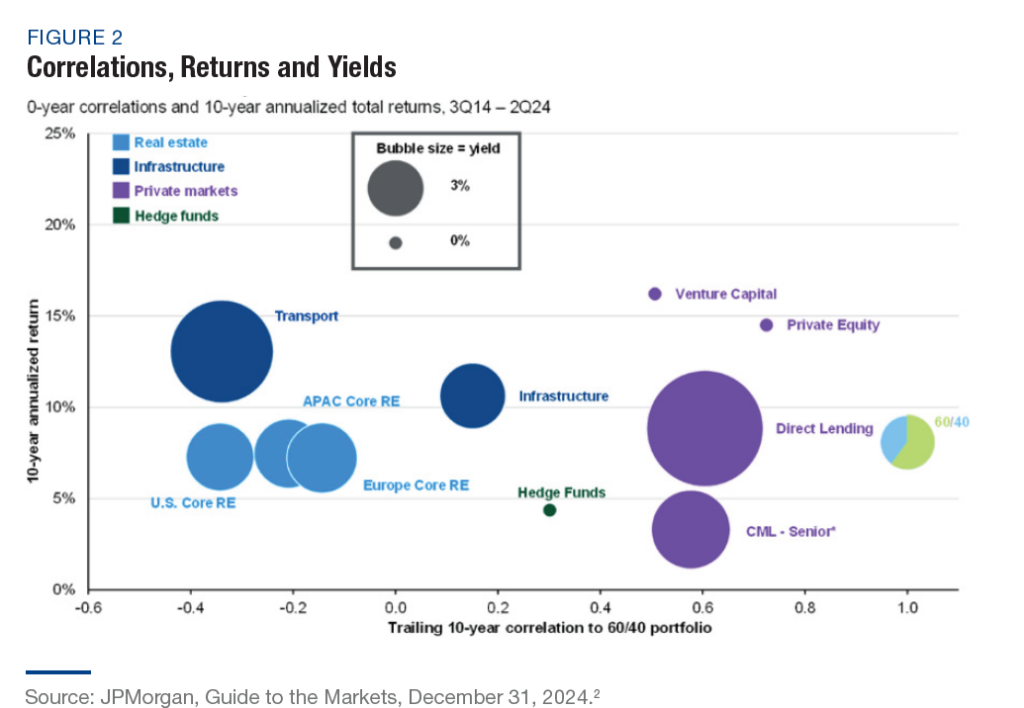

They offer the potentially superior returns of illiquid investments, such as real assets (e.g., real estate, energy, and infrastructure), or other private market investments, such as private equity and privatecredit (i.e., the illiquidity premium). Such investments often have the potential to offer higher yields than more liquid investments like individual equities or ETFs, making them attractive for long-term investors. Additionally, private market investments typically exhibit low-to-moderate correlation with traditional asset classes like stocks and bonds.2 This low correlation can provide valuable diversification benefits, helping to reduce overall portfolio risk and improve long-term investment outcomes.

Access to alternative asset classes (e.g., commercial real estate, infrastructure, energy, private equity, and private credit) can help investors capitalize on this illiquidity premium and the potential for higher returns while diversifying their portfolios with assets that often show favorable correlation to traditional markets.

1 https://pitchbook.com/news/articles/asset-managers-wealthy-investors-cliffwater

2 “Guide to the Markets, 1Q 2025 (as of 31 December 2024),” J.P. Morgan, https://am.jpmorgan.com/us/en/asset-management/adv/insights/market-insights/guide-to-the-markets/

Simplification and Efficiency

Interval funds can streamline tax reporting by providing investors with a 1099 tax form, a simpler tax filing option compared to the K-1 tax forms commonly issued by private partnerships. The intricate partnership-level calculations common in K-1s often increase tax preparation costs and typically require a tax filing extension. By contrast, the 1099 form enables straightforward and timely reporting for investors. This ease of use makes interval funds an attractive choice for those seeking private market exposure without the administrative complexity and burden often associated with traditional alternative investment vehicles.

Moreover, interval funds can offer significant tax advantages due to their structure. First, they avoid the double taxation typically faced by corporations where income is taxed at the entity level, and then again at the shareholder level when profits are distributed as dividends. Interval funds, however, pass through income and expenses directly to shareholders.

Second, the depreciation expense from the underlying holdings, if applicable to the interval fund’s investment assets, benefits shareholders by reducing the fund’s net income. This reduction allows a larger portion of the fund’s distributions to be classified as “return of capital” rather than ordinary income. Since return of capital is not subject to the same immediate tax rates as ordinary income, shareholders can defer taxes on that portion, helping to maximize after-tax returns.

Finally, interval funds are generally easy for financial advisors to allocate across their client base. Their ticker-traded structure allows for direct purchase through standard platforms without additional paperwork, enabling efficient execution at scale. This streamlined access to alternative investment strategies enhances the advisor’s overall value proposition.

Additional Considerations and Risks

Interval funds can provide access to private markets with a more operationally streamlined experience than traditional private funds, avoiding K-1 tax forms and the capital commitment and draw down structure typically associated with private placements. These features may make them suitable for investors seeking diversified alternative asset exposure through a structure that is administratively simpler than private placements.

While interval funds offer more liquidity than most private market vehicles, they still limit redemptions to periodic intervals, often with percentage caps. For this reason, they may be better suited for long-term investors who are comfortable with limited liquidity for a portion of their portfolio in exchange for the potential benefits of alternative asset exposure. Additionally, due to the complexities of managing private assets, interval funds may have higher fees than typical mutual funds.

It is important for investors to carefully evaluate a fund’s liquidity management practices, including its approach to maintaining a mix of liquid assets, access to credit facilities, stress testing, and conservative redemption policies. These practices can help manage liquidity risk, but investors who require ready access to capital should consider whether an interval fund’s redemption structure aligns with their needs.

Additionally, interval funds are subject to limitations on the types of assets they can hold directly, as they must primarily invest in securities. As a result, they may need to access certain private market investments indirectly (e.g., through REITs, partnerships, or holding companies) rather than holding them directly.

Takeaways (Interval Funds in Brief)

- Interval funds may offer a streamlined path to private markets, combining diversification, income, and inflation protection with structural transparency and periodic liquidity.

- Access to Private Markets: Interval funds can provide flexible access to investors looking for opportunities that are otherwise often available only through private (i.e., non 1940 Act) funds that have minimum investment thresholds of $5 million or more.

- Diversification: Interval funds can further diversify portfolios by including private market asset classes that frequently exhibit low correlation with traditional equity and fixed income markets.

- Inflation Protection: Interval fund investment strategies often target real assets like real estate, energy, and infrastructure, which often provide a natural hedge against inflation.

- Income Flow: Interval funds can invest in assets like real estate, infrastructure, and credit to deliver consistent, often tax efficient income to investors.

- Operational and Tax Simplification: Interval funds provide a straightforward 1099 tax form, simplifying the tax reporting process. They avoid the drawdown feature of many private placements and can typically be purchased via a ticker for maximum operational efficiency.

- Investor Protections: As 1940 Act vehicles, interval funds must comply with stringent regulations that ensure transparency, regular pricing, liquidity management, and clear investor communications. These safeguards offer a level of protection and oversight often not found in other private investment vehicles.